EDITOR’S NOTE: If you don’t read any further, apply these rules of thumb we found by looking at 10 years of super performance:

- Go with a fund that pays low fees, high fees is statistically correlated with worse performance.

- Go with an industry fund, as more industry funds have historically outperformed retail funds.

- And the fund that’s better than all the rest ironically is… REST. So you should start your search there.

In Australia, we all have money in our super. At 9.5% of your salary, it’s actually a lot of money that you probably don’t think about on a daily basis. But you probably should. On top of that, the law of time-value of money says a dollar today is worth more than a dollar tomorrow.

A critical player in all of this is the fund manager that looks after your money – or in other words your superannuation fund. And here’s the reason to care – depending on your choices here, it could mean the difference between doubling your money, or just keeping par. Retiring rich or perhaps relying on Government benefits.

Now, here’s the analysis.

———————

If you are on the ball enough to select the right superannuation fund early, you can make a lot of money over a 30 to 50 year investment throughout your working life. Even with minimum contributions, you can net a tidy nest egg by the time retirement rolls around.

Here is an example. Say you have accumulated $20,000 and you earn the median Australian full-time salary of $75,000 (these are the numbers we will be using throughout – obviously as you go through your working life and circumstances change, you might be earning less, or dramatically more than this). But let’s keep it simple.

With a mandatory contribution of 9.5% per year, you’ll put away $7,125 each year into your superannuation fund. Then, let’s suppose a mediocre returning fund with a rate of return (RoR) of 5%.

If we started our analysis at 30 (when you’ll likely have $20,000 in super accumulated and making $75,000 a year in salary), by the time your investment matures along thirty years later, how much money would you have? – $550,000.

The money you put in has doubled. That is the beauty of compounding interest.

Now, before you run away to just any super fund you come across, what if we told you that you could make twice this if you picked right, or drastically less if you picked wrongly.

We have analysed the Rate of Return, fees, and fund type for 29 of the largest superannuation funds (by funds under management) in Australia to determined which is historically best. More importantly we want to be able to give some guidelines on what to look for in a fund to make sure that you can choose the right one so that in 30 years’ time, you can afford the Ferrari hovercar you’ve always dreamed of.

Finding 1: Small Fees Actually Equal Bigger Return

Super funds are great at selling you the benefits of paying larger fees. People generally think ‘you get what you pay for’ – the higher fees, the better managed, better invested, and better looked after your money will be. But, that’s not what the actual data says.

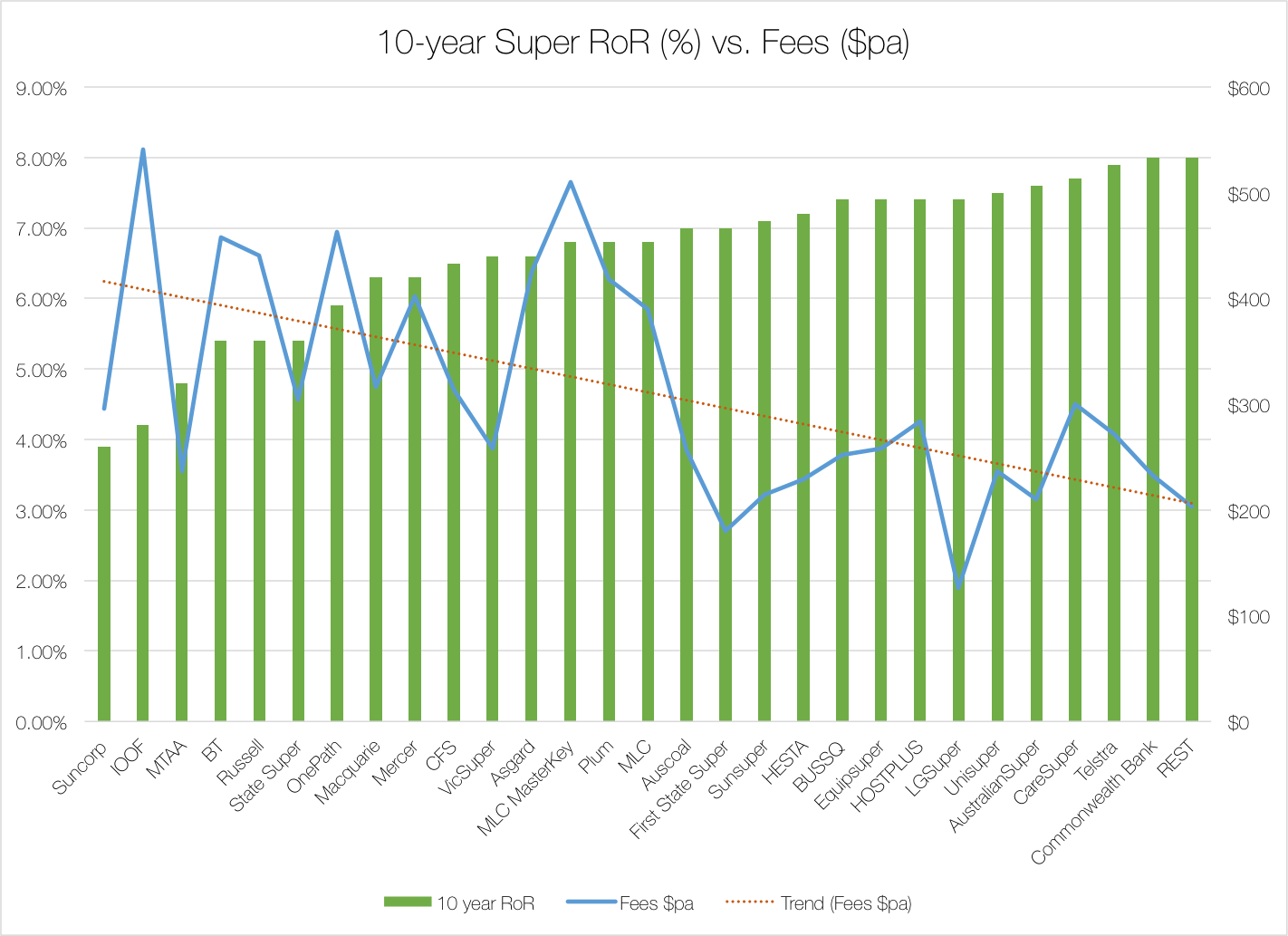

Look at Figure 1. This is the 10-year Rates of Return from the 29 funds arranged from lowest to highest 10-year RoR (green bars). From this you can see that an investment in the funds at the lower end of the spectrum (Suncorp, IOOF) are going to return a far smaller yield than those at the top end (Commonwealth Bank, REST).

The blue squiggly line are the associated fees for each fund. You will notice that as the green bars climb the blue line tumbles. We’ve added a handy ‘trendline’ (in orange( to show you the downward slope, in case it wasn’t obvious. What this shows is that the funds with the greatest return, the ones that are actually going to make you the most money over an investment lifetime, are also the ones with the lowest fees.

Finding 2: Superfunds Are All About The Long Game

Some funds will use something along the following lines to claim that their fund is better than others – The Rate of Return for this fund last year was 13.8%. – case in point. However, recent history shows, even with a window as small as 5 years, it’s hard to distinguish the good from the bad, let alone a single year. The top performing fund at 13.8% (IOOF Portfolio Service) did great in 2013, but horrible in 2012, when it had an RoR of -1.3%.

Figure 2 shows the same funds as Figure 1 arranged by their 5-year Rates of Return along with their fees (blue line). You can just about start to see the trend of low fees = high RoR, but this data is nowhere near as compelling. Nevertheless, even at 5 years, one thing is certain – paying more fees is a horrible indicator of better return performance.

For research purposes, the 10 year history is as good as you are going to find as a common criteria to assess.

Now, using that proxy, let’s consider two funds at different ends of the RoR spectrum. Suncorp has a 10-year Rate of Return of only 3.9%. That is, over the last ten years, this fund has averaged a 3.9% profit – in a decade where the RBA cash rate has been above 4% for the majority (i.e. they could have simply put it in bonds or high interest savings account and did better or the same – no work required). In comparison, the Retail Employee’s Superannuation Trust (REST) has an 8% Rate of Return for the last ten years.

What would happen if we extrapolated these rates out to our hypothecated investment above?

You have $20,000 to invest in either of these funds, and you plan to pay the minimum contribution from your $75,000 salary for each of the 30 years of the investment.

The difference is drastic.

Figure 3 shows the growth of your investment over the thirty years in each fund. REST trounces Suncorp as it reaches for the stratosphere. In this case, an investment with REST will see you taking home over a $1,000,000 for your retirement.

In the case of Suncorp, the same amount of money will net you only $450,000, half as much. Now that’s wealth creation!

Finding 3: Never Go Retail… Until Things Change

Finally, what types of fund are the best investment? This will probably change over time as the economy changes, but from our analysis of the last 10 years, industry funds are far outpacing retail funds in the current market. Figure 5 looks at the 10-year RoR again, this time with the bars colour-coded corresponding to fund type.

Industry and corporate funds seem to be the way to go in the current economic climate – the theory being that because these funds are operated to benefit only its members, they charge less fees compared to their retail counterparts.

It is also fascinating that the CBA corporate fund does far better than the retail CBA Colonial First State (CFS) fund. Is this purely a case of extra fees, or is it a difference in investment strategy? Anyhow, with regards to industry funds, these tv spots from a few years back had a real claim after all. Thanks Bernie!

Conclusion

So, what should you take away from this?

It certainly isn’t our intention to try and sell you one fund over another. In fact, some of the best funds in our analysis, such as the Local Government Super available in Queensland are obviously not available to everyone. More importantly, past performance is not necessarily a sign of future potential, and any one of these good funds might struggle come tomorrow.

Rather, it is important to show that, just because something is expensive doesn’t necessarily make it better. With super funds, any money you are paying in fees, for ostensibly better management or investing, would be put to far better use staying in your fund and growing with interest over time. At least that’s what history shows.

If you want that hovercar in 30 years, make sure you are looking for great rates of return, rather than paying someone a premium to look after your money.

Workings and data:

Most of the data was taken from ChantWest’s comparison tool (Fees; 2013, 5-year, and 10-year Rates of Return; and fund type). Where 10-year Rates of Return were not available on this tool, those were taken from the Australian Prudential Regulation Authority’s Superannuation Fund-level Rates of Return publication, June 2013.

An interesting read. A couple of brief points: – Superannuation is not just fees and performance. If you don’t consider insurance arrangements within the super environment, you’re missing out – It is also fair to say that the cost of this insurance should be part of a holistic view in determining the ‘best’ fund.

– Recent data suggests that insurance premiums are higher in some industry funds, as a result of claims experience, and broad acceptance of members.

– There are a number of investment options/funds without 10 year performance data. (eg. A number of newer options opened specifically to meet ”MySuper” requirements are still less than 12 months old)

– Additionally, although Industry funds often have less expensive fees when compared to retail offerings, this is not the case when comparing tailored rates for Corporate plans. You should check the fees/charges/insurance premiums offered by the default fund where you work – Often larger groups can negotiate significant discounts.

Hi Andrew,

Thanks for your feedback.

All of your points are completely correct. I didn’t include the insurance costs of each fund as the data was incomplete for the top funds.

Additionally, as you say, the 10 year, and 5 year, RoRs aren’t available for a number of funds either. The top supers in terms of assets were chosen here, but this data might look different in a few years time with newer funds. Also, as you say, some people might find that specific funds they have access to will have better returns than general supers available.

Cheers,

Andrew

Is this analysis based solely on the default investment option for each fund? Comparing returns across funds is complicated by different definitions of ‘balanced’.

Hi Luke,

I looked at growth assets when comparing the funds. You are correct that what might be classified as ‘balanced’ or ‘growth’ for one fund might not be so for the next, but the APRA have found that there are no long term differences between growth and balanced default options for most funds.

http://www.apra.gov.au/AboutAPRA/WorkingAtAPRA/Documents/APRA-Summary-Article-Final-050109_LynMcDougall_with-cover.pdf

Cheers,

Andrew