Every Friday night, from Perth to Parramatta, millions of Australians knock-off work with a thirst that only their favourite drink can quench. Whether it’s a schooner from the local, a bottle of merlot shared on the balcony or – quite a bit later in the evening – a shot of tequila before striding to the dance floor, it is no secret that the majority of Australians enjoy a drink in their free time.

At Pocketbook we were curious to see exactly how much Australians were spending on booze.

While the consequences of excessive alcohol consumption can be tragic and are known to lead to wider societal issues (according to Australian Institute of Criminology’s 2013 report The societal costs of alcohol misuse in Australia, alcohol-related problems cost society more than an estimated $14 billion), we wanted to explore how our drinking culture was hitting Australians’ hip pocket.

By analysing the spending habits of Pocketbook’s 250,000 users, our aim was to provide insights into the trends and patterns associated with alcohol consumption in Australia, which could in turn be used to predict future spending. As always, we analysed the data in aggregate and with identifiable information removed.

During our research, we split spending behaviours into three different categories: Big Box retailers (Dan Murphy’s, First Choice, BWS etc.), Small Box retailers (smaller wine and liquor shops as well as specific online retailers such as Jimmy Brings and Cellarmasters) and Bars/Pubs. With a final aggregate sample size of 128,192, we reviewed spending habits for 2014, 2015 and 2016.

Our investigations began with a few common sense hypotheses like Australians spend more on alcohol over Australia Day than they would over the course of a normal weekend (save the sarcasm – we told you these were common sense hypotheses!).

We also hypothesised that Australians were spending more on alcohol year-on-year, essentially in parallel with general consumer spending trends.

While some of our hypotheses were spot on, you might be surprised at the findings that ran counter to our predictions.

We’ll leave a deeper analysis of these trends, along with the industry context, to others, but here’s some of the key findings from our data:

- Australian spending on alcohol has remained relatively steady over the past three years. While there has been a slight year-on-year increase, the average monthly spend per person in the 2014, 2015 and 2016 financial years was $113.03, $121.43 and $124.45 respectively. Have we reached “Peak Alcohol” as a nation? Or are awareness-raising efforts like febfast having an effect?

- Smaller retailers are struggling. Since 2014, smaller retailers have experienced a decline in market share every year while the spend at both Big Box and Bars/Pubs has been increasing.

- Dominant players continue dominate. During every year analysed, Dan Murphy’s had close to double the market share of its closest big box competitor. Interestingly, Liquorland experienced a resurgence, more than doubling its market share since 2014 (from 11.28% in 2014 to 23.28% in 2016).

- The number of tipples triples on Australia Day. During the Australia Day period, the number of people purchasing alcohol increased by at least 3x every year. Interestingly, this also causes a shift in the spending spread between Big Box, Small Box and Bars/Pubs – more on this below.

- On Australia Day, the average spend per person is LESS than on an average weekend. This one took us by surprise, but it makes sense when you consider the influx of occasional drinkers purchasing lower amounts for the occasion thereby bringing down the average spend across the board.

- The festive season is thirsty work. Australians are spending an average of 25% more on alcohol during December than the rest of the year – this rate has also been increasing steadily over the past three years.

- Australia Day is spent outdoors. Patronage at bars and pubs more than halves during Australia Day, while spending at bottle shops of all sizes increases. It’s hard to beat the backyard barbecue or a day at the beach on Australia Day.

|

Now for the numbers…

Alcohol Spending Analysis

We conducted a study into Australian spending on alcohol over the past 3 years with specific focus on December to January festive season spending, and also for the Australia Day period over 2014, 2015 and 2016.

As part of the study, we looked at spending for the following alcohol retailers:

Big-box retailers:

- BWS

- Cellarbrations

- Dan Murphy’s

- IGA Liquor

- Liquorland

- Woolworths Liquor

- Bottlemart

- Vintage Cellars

Small-box retailers both online and offline, using keywords:

- Other bottle shops

- Other liquor shops

- Other wine shops

- Specific online retailers such as (Vinomofo, Cellarmasters, Jimmy Brings etc)

Bars and pubs including suburban hotels, pubs, bars.

The sample size for the study is 128,192 people.

Hypothesis 1: Australians are spending more year-on-year on alcohol.

Australian spending on alcohol has remained relatively steady yearly. We looked at monthly average spending per person for the past 3 years.

- 2013-14 – $113.03

- 2014-15 – $121.43

- 2015-16 – $124.45

While this is the case, the makeup of the spend across types of retailers has only shifted slightly – with small-box stores declining;

- 2013-14: 43% Big-box , 33% Small-box, 24% Pubs/bars

- 2014 -15: 45% Big-box , 30% Small-box, 25% Pubs/bars

- 2015 -16: 45% Big-box , 29% Small-box, 26% Pubs/bars

Some insights:

- Big-box is almost half of the spending in dollar terms

- Small-box has shifted 4% less over the last 3 years (Could this be because people going out more? Big retailers taking over share? – Further research is recommended).

Of the Big Box group, the following are the best The best performing liquor stores Liquor Stores:

- Dan Murphy with a market share of 45.17% (down from 50.13% in 2014)

- Liquorland with a market share of 23.28% (up from 11.28% in 2014)

- BWS with a market share of 22.95% (down from 27.19% in 2014)

Note: The rest of the big retailers growth was relatively stable.

One of the reasons why Big Box group might be taking over is due to the discounts they’d likely offer over smaller vendors. An early evidence of this is that for the year Dec 2014 to Nov 2015, the average transaction amount is 25% higher at small-box stores smaller retailers. Further analysis is recommended based on like-for-like product price comparisons.

- Big-box – $44.73 average transaction size

- Small-box – $56.16 average transaction size

- Bars / Pubs – $36.64 average transaction size

The average transaction size appears to line up well with the average expected prices for 1x case of beer, 1x bottle of spirits or 2-3x bottles of wine.

Hypothesis 2: Australians spend more the Australia day period versus the average weekend

During the Australia day period – there is an overwhelming amount of people purchasing alcohol compared to an average weekend. The amount of people increase in amount of people purchasing alcohol over Australia day is between 3-4 times the typical weekend.

- 2014 – 3.06x

- 2015 – 3.79x

- 2016 – 4.20x

We then looked at how the spending on Australia Bay varies by retailers types. The makeup in spending also changes during the Australia Day period versus a regular weekend for 2014-15.

- Big Box – Down 48.65% to 43.81% on Australia Day.

- Small Box – Up 28.08% to 35.24% on Australia Day.

- Pubs/bars – Down 23.27% to 20.94% on Australia Day.

Some insights:

- Less people are spending at Big Box retailers and more people spending at Small Box retailers.

Despite the huge increase of people spending on alcohol, the average transaction size remains consistent to the average weekend, so the typical purchase is very much still 1x case of beer, 1x bottle of spirits or 2-3x bottles of wine:

- 2014 – $47.87 Australia Day, $48.16 Regular Weekend

- 2015 – $48.52 Australia Day, $45.48 Regular Weekend

- 2016 -$43.43 Australia Day, $44.69 Regular Weekend

Hypothesis 3: Australians spend much more on alcohol over the December / January festive season.

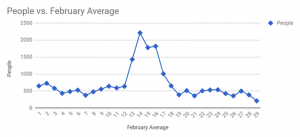

During the December period there is huge jump in spending followed by a steep decline in January and February. This can be seen by looking at the total average monthly spend per person. This is an expected decline as December is the festive season.

| Average per person spend Dec to Feb |

2014 (Dec 13) |

2015 (Dec 14) |

2016 (Dec 15) |

| December |

$135.85 |

$150.37 |

$153.30 |

| January |

$107.14 |

$117.47 |

$116.93 |

| February |

$102.50 |

$109.11 |

$116.50 |

We can see here that the average spend per person is much higher during the month of the December period:

- 2014 (Dec 13) – $135.85 – 22.4% above monthly average (excluding Dec)

- 2015 (Dec 14) – $150.37 – 26.58% above monthly average (excluding Dec)

- 2016 (Dec 15) – $153.30 – 28.96% above monthly average (excluding Dec)

Similarly, there is a reduction of monthly spend in February. People are likely putting into effect their new-year’s resolutions (ie cutting down alcohol consumption or saving money) – more research needed.

- 2014 – $102.50 – 8.20% below monthly average (excluding Dec)

- 2015 – $109.11 – 8.88% below monthly average (excluding Dec)

- 2016 – $116.50 – 2.04% below monthly average (excluding Dec)

Finally, we looked at the drop-off for specific store types. We noticed that the bigger the store (ie the more planned purchase) the bigger the drop-off between December to February. This means the Big Box stores drop off the most and bars the least.

- Big box – 29%

- Small box – 13%

- Pubs/bars – 10%

| Average per person spend December – February: |

Month |

2014 (Dec 13) |

2015 (Dec 14) |

2016 (Dec 15) |

3 year average |

| Big Box |

Dec |

$110.11 |

$115.69 |

$119.61 |

$115.14 |

|

Jan |

$80.97 |

$85.58 |

$86.42 |

$84.32 |

|

Feb |

$77.51 |

$82.77 |

$85.90 |

$82.06 |

| Small box |

Dec |

$99.10 |

$111.74 |

$105.37 |

$105.40 |

|

Jan |

$86.81 |

$98.71 |

$89.16 |

$91.56 |

|

Feb |

$87.63 |

$92.82 |

$93.74 |

$91.40 |

| Pubs/bars |

Dec |

$75.28 |

$78.42 |

$77.19 |

$76.96 |

|

Jan |

$71.78 |

$71.27 |

$72.16 |

$71.74 |

|

Feb |

$68.78 |

$68.90 |

$70.61 |

$69.43 |

We can see that the the biggest drop off in per person spend is at big box retailers. The smallest drop-off is for pubs/bars.

Pocketbook Personal Spending Takeaways.

The above findings should give you a leg up when it comes to how you spend your money on alcohol. And here are three additional key takeaways:

- Consider doing FebFast. Chances are, you’re spending less on alcohol in Feb. Why not do it for a great cause. Get sponsored for your behaviour change and raise money to help disadvantaged youths in Australia.

- Visit a “Big Box” retailer. The numbers suggest that many more people are now flocking to Big Box stores, most likely to take advantage of the discounts they are able to provide. But if you are aiming to reduce spending, plan ahead and you could save more. The bottleshop next to the pub may be convenient by being open at 8pm on your way to a house party, but chances are it’ll cost you more than an afternoon trip to Dan Murphy’s.

- Remember to budget more dollars for drinks during the festive season. Spending on alcohol (and many other things) goes way up during this time, so take a lesson from the numbers above and set a budget based with them in mind.

Wishing you a happy Feb(fast)!

|