Bank fees are sneaky!

Whenever looking at my transactions online, I always find myself balling my fist and gesturing in rage. All these poorly reasoned and described fees! I wish there was a simple way to react in real time.

Here’s a quick list of some fees I hate.

Foreign Exchange Fees: This one kills me when I travel overseas. However, what’s more annoying is that with my online purchases increasing over the years, this fee (up to 5% of total transaction value) has steadily increased.

Transaction Processing Fees: Most banking products limit the number of transactions per week or month. This means, whenever I go over these limits, I get charged.

Cash Advancement Fees: As a frequent credit card user, I sometimes mistakingly withdraw cash from my credit card at the ATM. This wacks me with a fee of up-to $15 per transaction.

Minimum Balance Fees: Some savings accounts have minimum balance requirements. These fees have become less common over the years. I used to have to make sure there’s enough money in my savings account at the end of every month.

Monthly or Annual Fees: This applies to almost all my accounts. The biggest surprise for me always is my annual mortgage package fees. Typically a big $400 hit when I least expect it.

Overdraft Fees: This is where deductions are made from my account despite there not being enough funds. This typically happens with direct debit bill payments, charging up to $30 to $40 per violation.

Account Closing Fees: Some banks also charge a nominal fee to close an account. However these are also becoming less common.

Tips to minimise fees

If you’re just like me, I’m sure you can use these tips I’ve gathered for minimising fees:

1) Read the terms and conditions for the account carefully, and get special exemptions (ie waived annual fee offered to you only) in writing from your bank representative or broker, before you sign.

2) Monitor transaction history periodically to make sure they reflect the arrangements you agreed to when purchasing the product.

3) Get educated about competitor products to discover those that may suit your lifestyle better. For example, if you’re becoming a frequent online shopper or travelling more overseas, a credit card with less or no FX transaction fees start to make more sense.

How Pocketbook helps with minimising fees

Pocketbook can help you today in a number of ways:

1) Automatically tagging bank fees as transaction history is updated. This not only allows you to discover new charges, but also gives a quick view of totals so you can do more analysis.

2) Automatically tagging monthly fee commitments as “bills”, so you no longer are surprised by the timing of these charges.

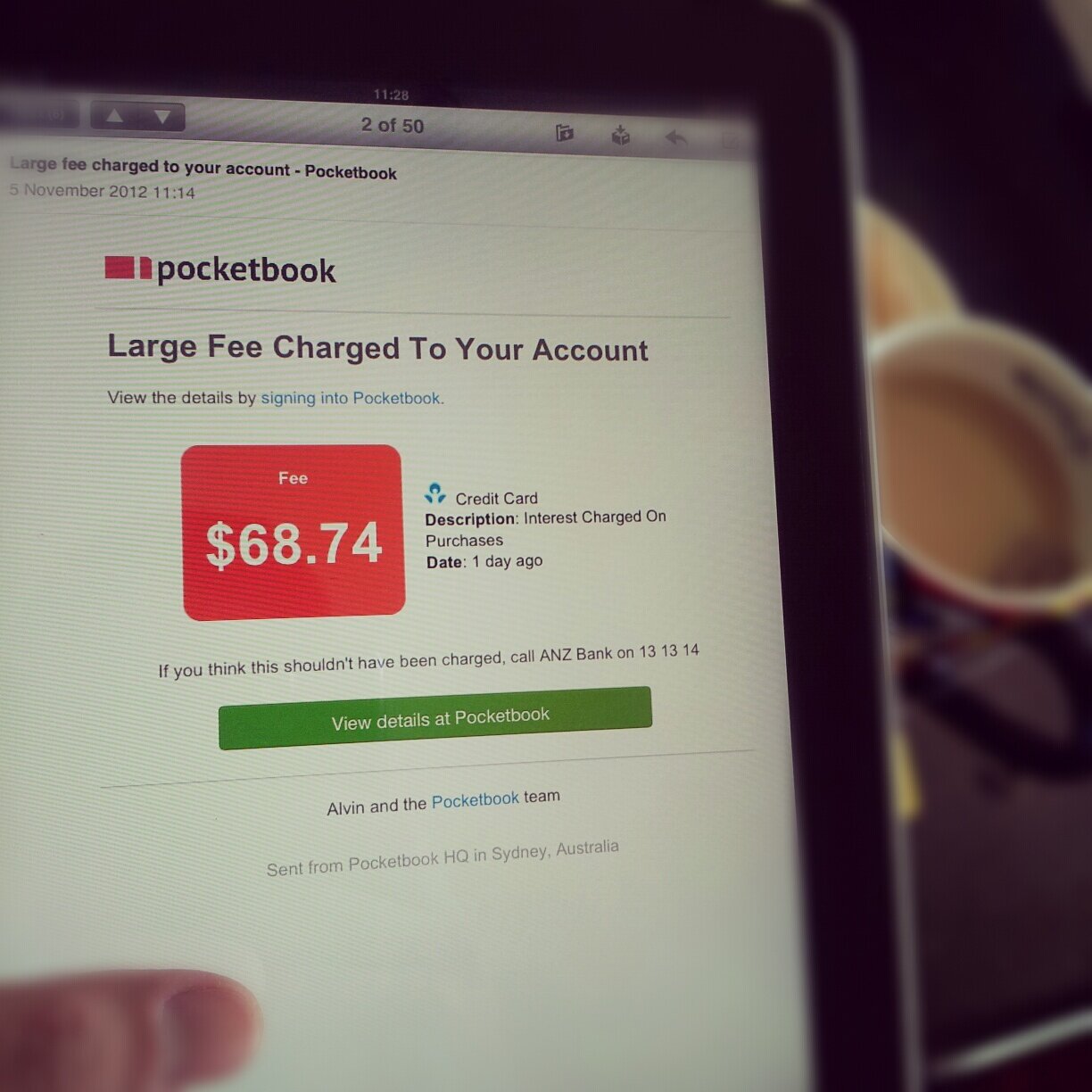

3) Sending alerts to your email when bank fees are significant in real-time. Providing you with the name of the account, the label on the transaction, as well as the bank’s service number (see picture above). Allowing you to deal with the bank in real-time where a fee is unjust.

Just some of the ways we’re making managing bank fees and personal finance ridiculously simple for you!

Bosco