It’s an age old debate – rent or buy your house.

The great Australian dream says buying is always better – it is the key to financial freedom. However, over the course of 2013, we’ve seen property prices skyrocket, particularly in Sydney. Median house prices have now reached $700,000, while average rental prices have stayed relatively steady at $500 per week.

The 1:1 litmus test

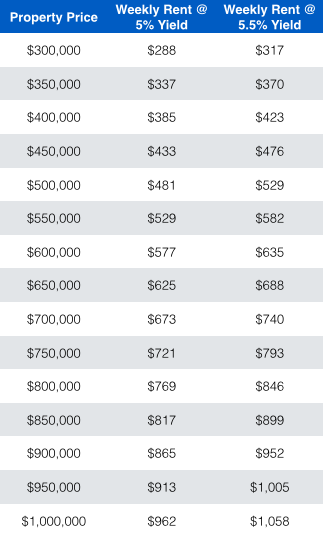

Property investors typically talk about yield – the regular return you could expect from an investment. For instance, if rental income is $500 a week, and the purchase price is $500,000, then yield would be ($500 a week rent * 52 weeks) / $500,000 = 5.2%.

Investors typically target a 5 – 5.5% yield at a minimum with today’s interest rate (~6%). This means for a $500k property, a rental income of $481 to $529 would be considered acceptable. The reason for this relates to the interest payment (and not really on the principle repayment – more on this later).

For a $500k property, assuming a 10% deposit and 25 years to repay, the expected interest payment on the loan is $519 a week – as you can see, this sits nicely in desired yield range. So in this instance, the rent covers the interest, leaving the investor free to pay off the principal.

Why does this work for the rent or buy decision

The reason this works because paying rent is just like paying interest only. The outcome is the same – you don’t actually end up owning any of the property. In the investment sense, it is only when you start paying off the principal of your borrowing that you start owning a slice of your house. Obviously there are considerations to be made in terms of paying off the principle (you can also use the interest only loan) and cash-flow. Essentially, an investor is looking for capital growth (i.e. house prices going up) while maintaining cash-flow.

Let’s do some maths with real Sydney suburbs…

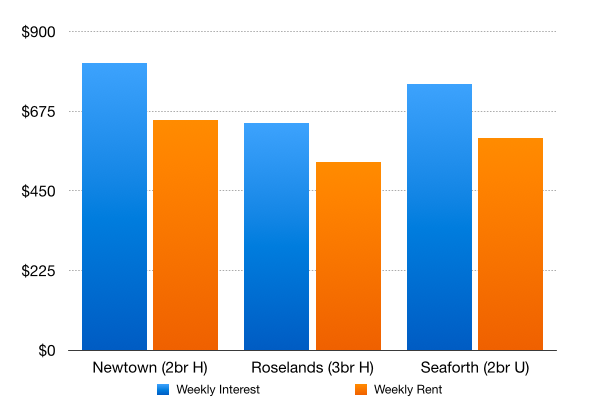

Let’s start with Newtown (2042) – a vibrant inner city suburb with easy public transport and a bohemian culture. The average price for a 2 bedroom house is $781,000 to buy. A 5% to 5.5% yield works out to be $751 to $826 – which is well above the expected rent of $650 for a similarly sized property.

Next – let’s look at Roselands (2196) – a working class inner west suburb, with public transport at its edges and a multi-cultural mix of young families. A 3 bedroom house is $618,000 to buy. The average rent expectation of $530 is still short of the yield expectation of $594 to $654.

Finally, Seaforth (2092) – a wealthy Northern Beaches suburb in Prime Minister Abbot’s electorate of Warringah. A 2 bedroom unit here costs $725,000 to buy. So again, a rental expectation of $600 is well short of the $697 to $767.

In fact for every suburb scenario, the interest repayments are 20% more than rent. See chart.

So is it buy or rent?

Analysts suggest Sydney property prices are expected to increase 19% over the next 3 years. With Perth and Brisbane not too far behind. So chances are, if you want to own your own place, then it won’t get any more affordable. Bite the bullet and make room for the extra 20% you’ll spend on housing week to week. Pocketbook can help you track it!

If you don’t care about owning your place, then bank on rental prices increasing slowing relatively speaking. That way it’ll actually be more and more affordable to rent come 2016.

Bosco

You can see a list of expected yields at 5% to 5.5% for your easy reference.