Sephora is one the world’s largest cosmetic retail chains. With almost 2,000 stores in 29 countries, the French company is part of the Louis Vuitton luxury goods group and has annual revenues of €1.94 billion. And now for it’s next global expansion it has set its sights on Australia.

The company opened its first Australian flagship store in Sydney on 5th December 2014, just in time for the Christmas rush and Boxing day sales. The store is located at 188 Pitt Street Mall, in Sydney CBD’s main shopping district. This geographic choice is highly strategic, opposite big department stores (Myer & David Jones), next to fast-fashion poster-child Zara and a stone’s throw away from super-pharmacies (Soul Pattinson and Priceline) that along with the department stores – have long dominated the cosmetic and beauty sectors within the city’s centre, and indeed the rest of the country.

Similar to what Zara and Topshop did to women’s fashion in the same physical location 2 years ago, Sephora is looming to disrupt the competitiveness of health and beauty.

The department stores today each dedicate entire floors to cosmetics brands, typically at the entry or ground floor level. And it’s terrific business to do so. In fact, Macquarie Bank research estimates that the cosmetics sales for Myer’s Sydney CBD store alone makes up to around 1 to 2% of the total Myer annual sales revenue – a big contribution given there’s around 60+ stores across Australia and 7 other key departments.

Sephora meanwhile, is targeting a 10% share of the $4 billion Australian cosmetics market, a mark they hit in only 3 years in Singapore and Malaysia.

So with a big fight on the cards, we decided to analyse the Australian consumer reaction to Sephora within the Pitt Street Mall radius. Focussing specifically on Myer, David Jones, Soul Pattinson and Priceline Sydney CBD stores, alongside Sephora for the span of December (Dec 1 to Dec 29).

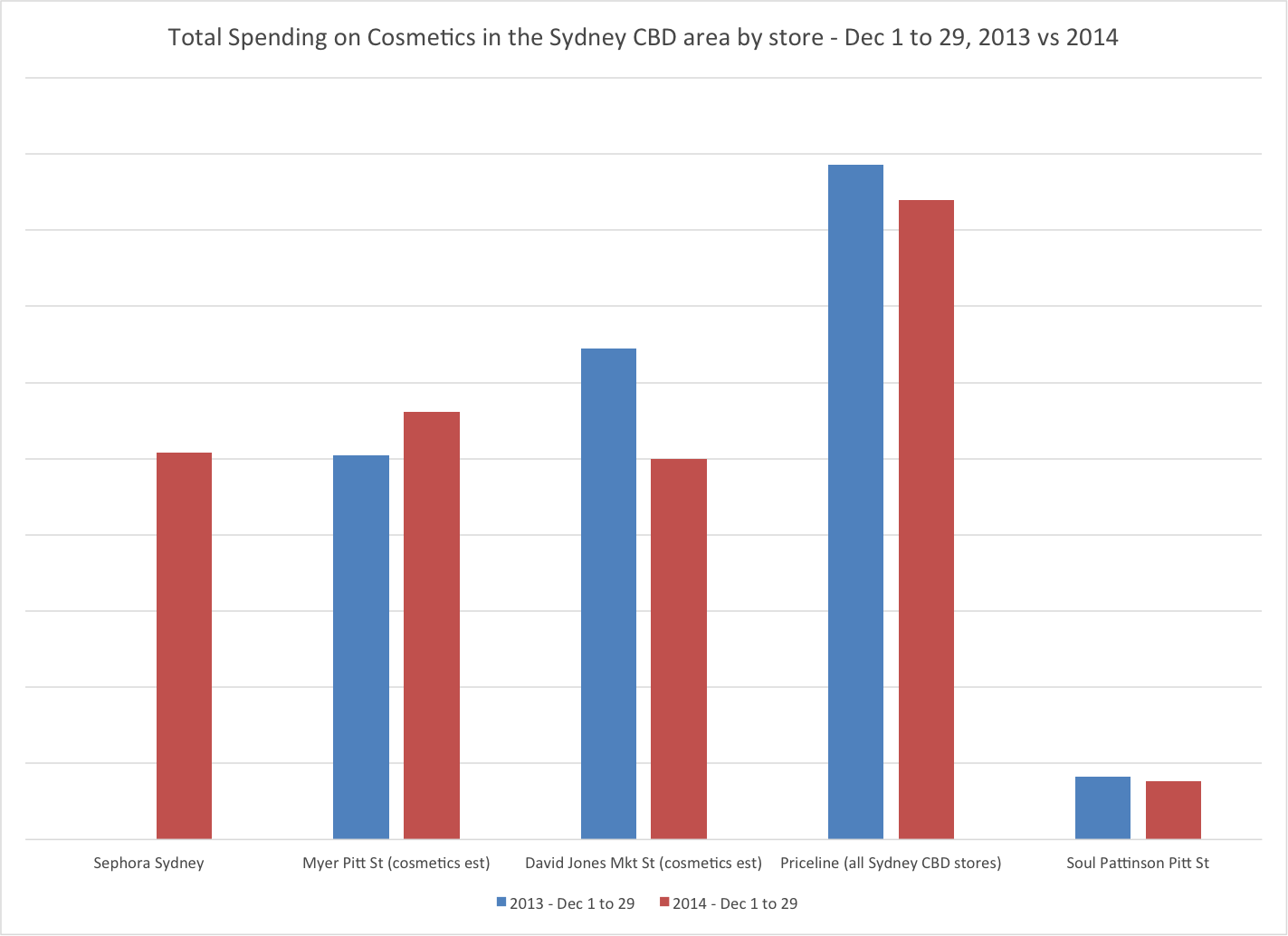

Sephora is already making its mark as a Pitt Street mainstay

Using Macquarie Bank’s 1-2% assumption, we estimate that in 2013, the cosmetics contribution for the Myer city store total sales is around 13%. We use this proxy for both Myer and David Jones for representing cosmetics. This is the result for the first 29 days of December.

This shows that Sydneysiders have taken to Sephora in a big way in the period. The total spending outpaces David Jones, and is about two-thirds of all spending at the 10 CBD Priceline stores combined.

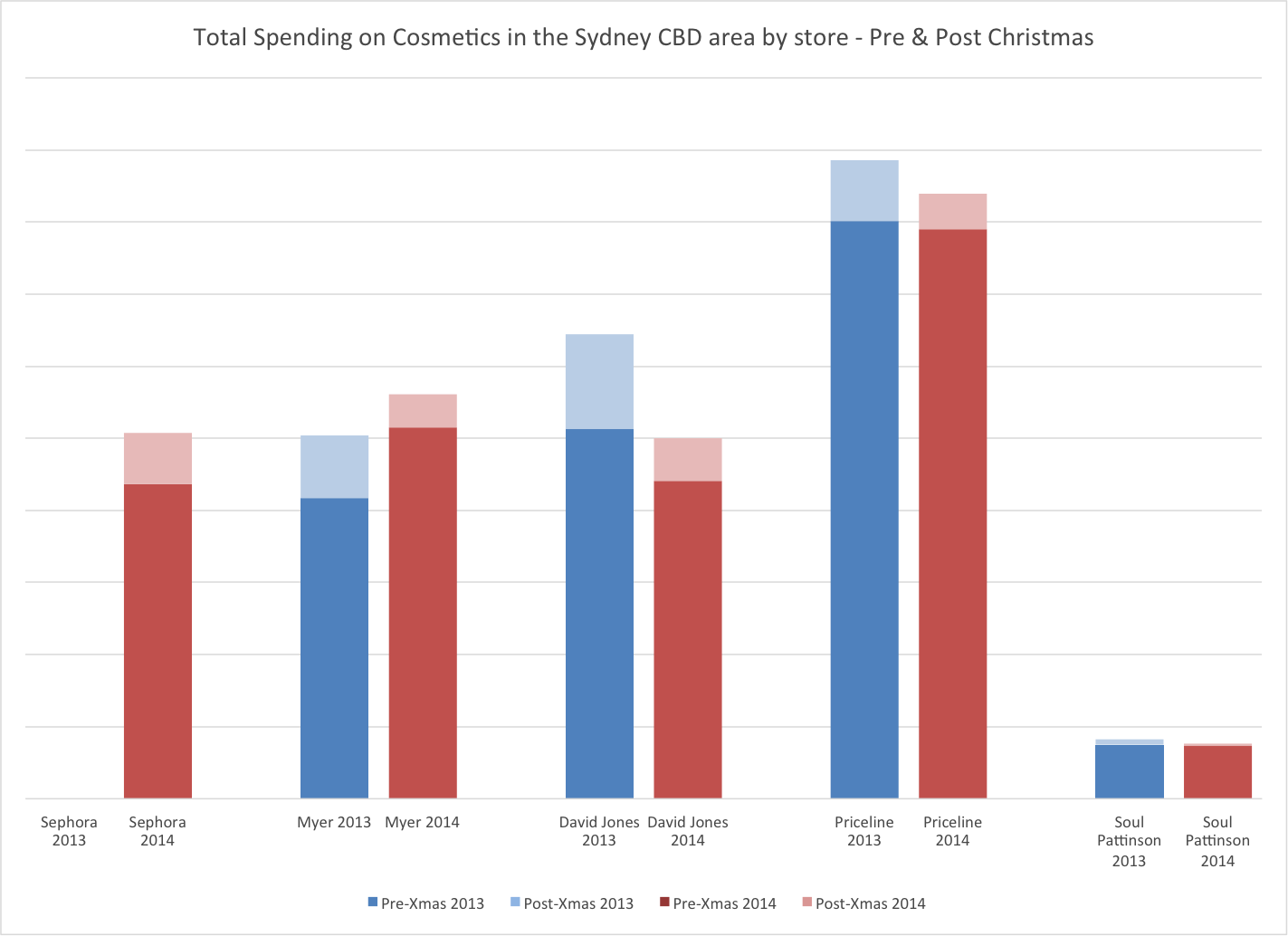

When we split this result out to pre and post Christmas spending, what we find is that in the 5 days post Christmas, Sephora is still achieving a result that outpaces all its competitors. Around 54% more than Myer, 20% more than David Jones and 44% more than Priceline.

This means that in just a month, Sephora has been able to establish itself significantly. While it has not totally decimated others, the story of the final 5 days is more impressive than the first 24 (note that Sephora opened on the 5th – giving other retailers a 5 day headstart as well).

We anticipate this steep pace to grow significantly in the coming months. Particularly as one of Sephora’s key strategies is to release a new product every month when they open a new market.

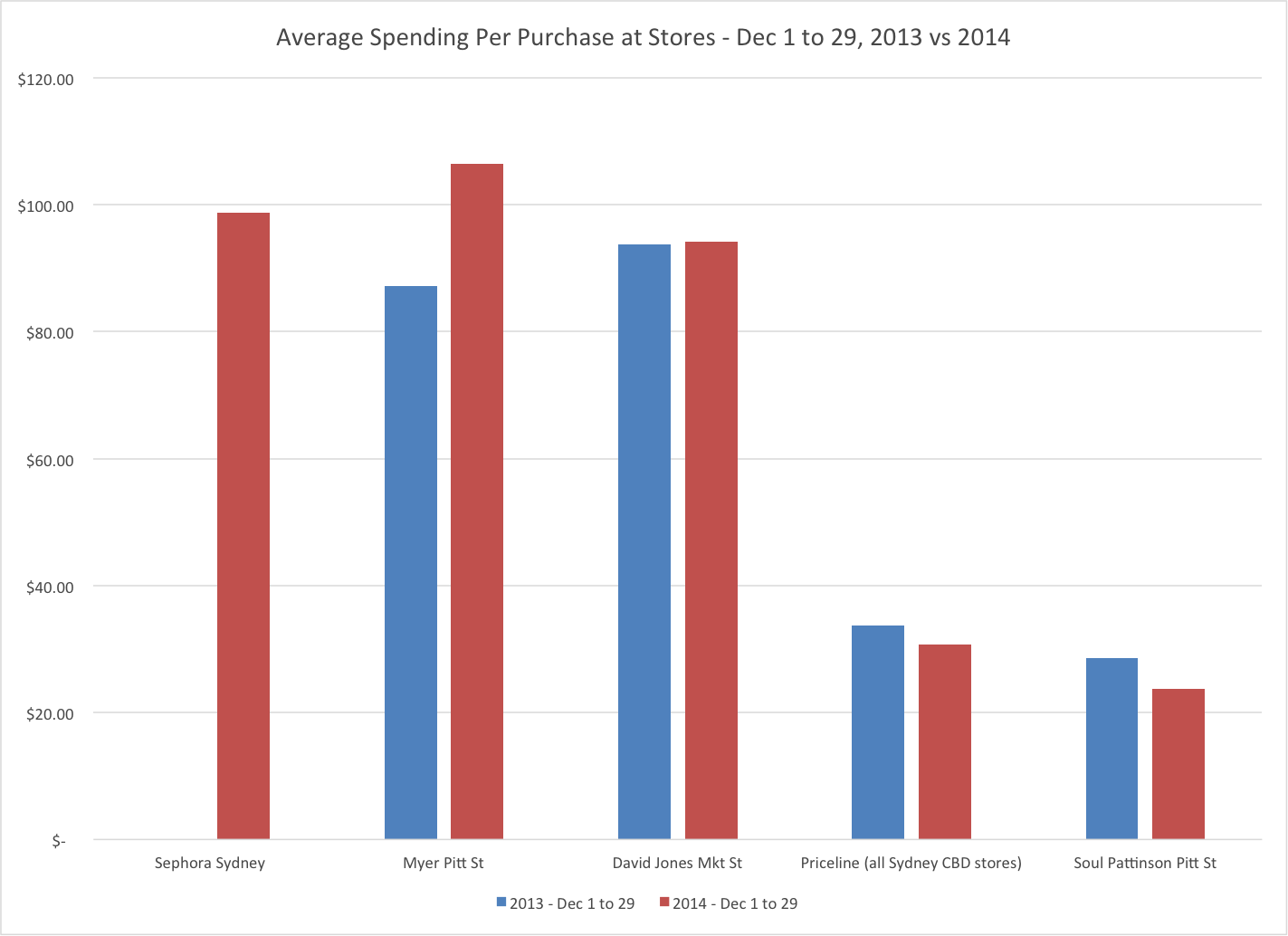

People spend as much at Sephora as at Myer and David Jones

Another reason why the incumbent retailers should be worried is the average purchase value. Sephora also isn’t just getting more people through the door, but each person is spending a whole lot every time they shop.

When we look at this, the average basket of $98 is on par with both Myer and David Jones. While people do over-spend at new store openings, it is seemingly unfathomable that a cosmetics retailer can sell more per transaction than a retailer than sells designer label fashion, homewares and electronics.

However, the good news for the department stores is that customers seem to be more in the “stocking up” mode. Meaning revisit rates aren’t as high as the department stores. Time will tell of Sephora settles to be more like Myer or more like Priceline in the months to come.

Super-pharmacies might indeed be the first to buckle

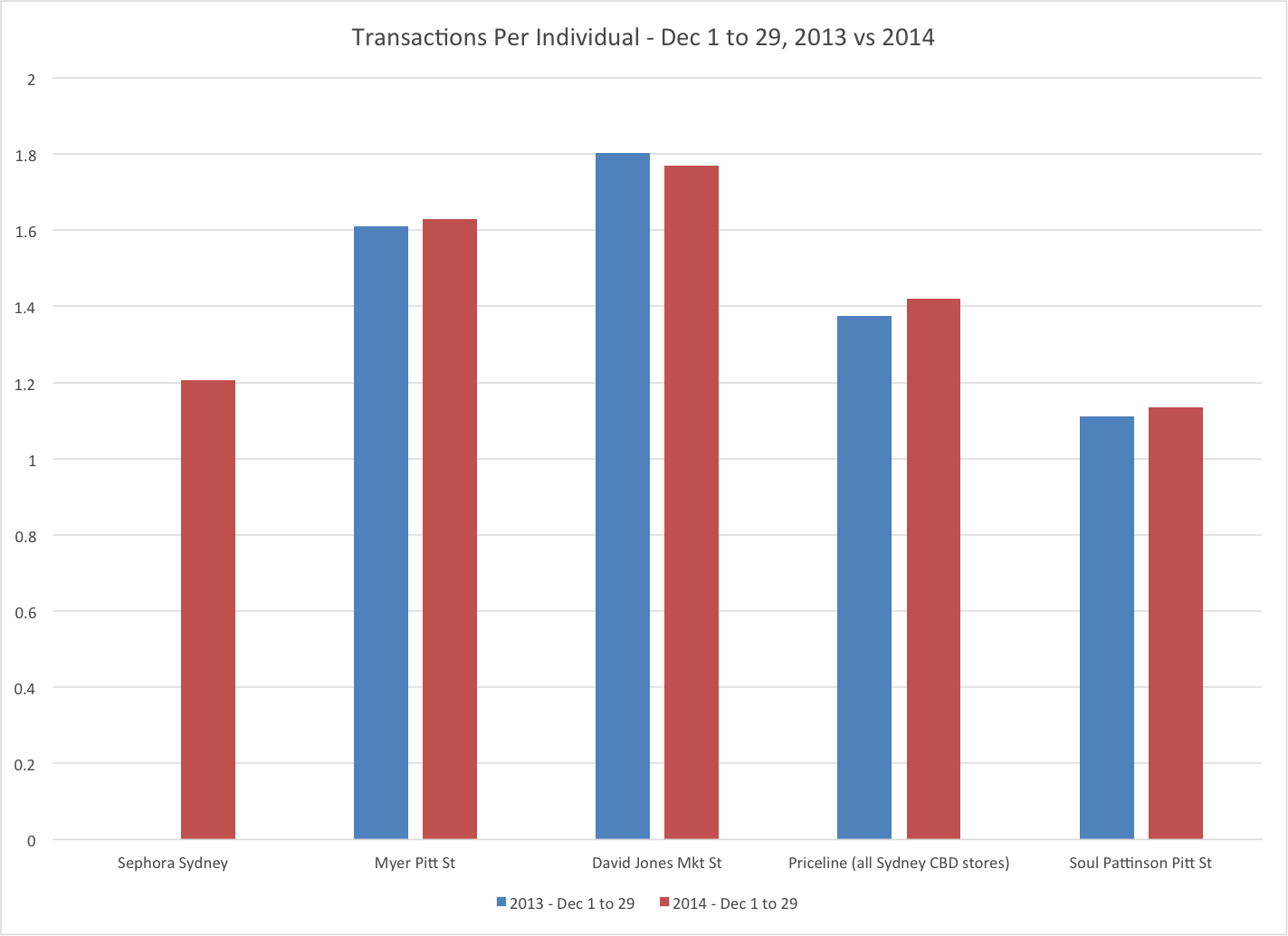

While a lot of early media and analyst focus has been given to Myer and David Jones in terms of the Sephora impact, the more impending concern might be the super-pharmacies, like Priceline.

Both owned by the same parent Australian Pharmaceutical Industries, Priceline (10 stores in CBD) and Soul Pattinson (160 Pitt Street, just a few shopfronts down from Sephora) run a group of full-range “health and beauty” focussed pharmacies in Sydney’s CBD. These are more than just classic suburban chemists and draw a lot of foot-traffic and sales from its personal care and cosmetics lines. To date, they don’t just compete with the department stores for higher value cosmetics customers, but also the 600 other smaller pharmacies in the Sydney CBD area – that are typically focussed on the their dispensary functions (prescription medicine).

The hypothesis is that as competition for the higher value beauty segment intensifies, the viability of these stores may come under pressure.

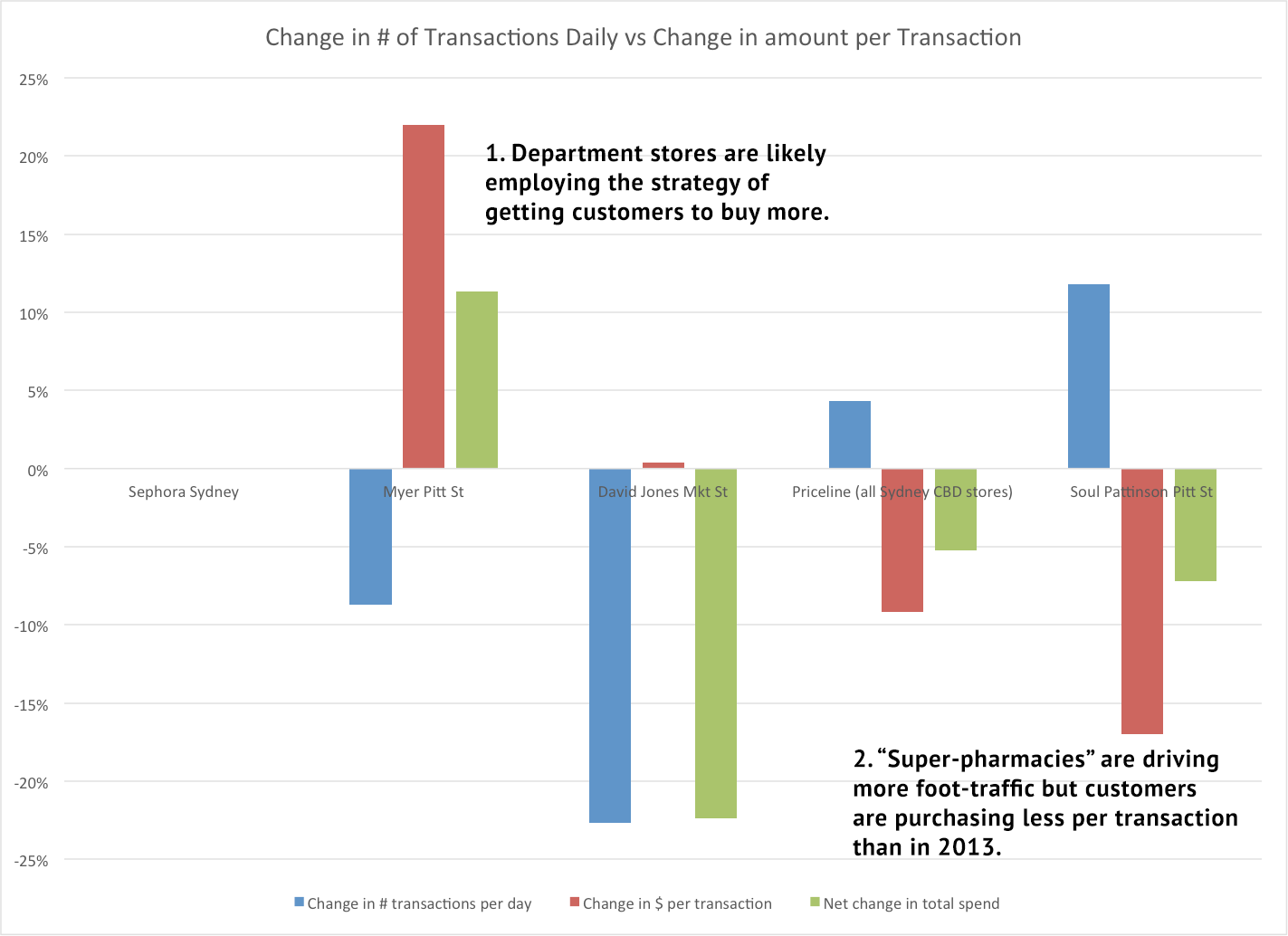

Indeed, when we look at the change in number of transactions and average spend, the impact on the department stores and the super-pharmacies are very different. The department stores are challenged by less traffic, but compensated with higher spending per transaction. Meanwhile, the reverse is the case for Priceline and Soul Pattinson.

Given the range and store layout, Priceline and Soul Pattinson may find it difficult to up-sell customers that come in for small purchases. Particularly with Sephora down the road. Additionally, any desire to perhaps tackle the competition on price may be rebuffed by Sephora’s reactions to the recent “Australian Tax” pricing criticism.

In contrast, the department stores have more room to absorb the competition, and more floorspace and range to try to up-sell, as the data already appears to show.

Conclusion

Though a global success, Sephora is not without its failures, with withdrawals from markets in Japan and Germany. Whether it will succeed in Australia like in Singapore or the US remains to be seen. Sephora has a lofty target of a 10% share of the Australian cosmetics market, and on the strength of this data dominated by the likes of Myer and Priceline, their initial execution to take the competition head on seems to be on the money.

Our Data

- Our data comes from the real-spending of Pocketbook users, with all data de-identified, aggregated and analysed internally to protect security and privacy of our users data.

- We have 100,000+ Aussies using our app. Out of that batch of 100,000, we sampled 60,000 of them for this study. We do this by using a method called k-means clustering.

- Using analysis from Macquarie, we estimated that 13% of all spending by Pocketbook users in Myer and David Jones Sydney CBD stores was from the cosmetic department and adjusted our data accordingly.