Value investing is the practice of selecting stocks that trade for less than their intrinsic value. The idea is that these stocks are undervalued in the current market but will become more valuable in the future. The result is an opportunity for value investors to profit by buying when the price is deflated. As opposed to investors who respond “emotionally” to market trends, buying at the first sign of a high and selling at the first sign of a low, value investors respond “rationally” to trends, considering stock price movements in terms of a company’s long-term fundamentals. They understand that even good companies face setbacks. Just because a company is struggling doesn’t mean that it isn’t still fundamentally valuable or that its stock won’t bounce back. Value investors turn setbacks into profit opportunities by considering a company’s long-term value and ability to recover. Warren Buffet, one of the world’s most successful value investors, once said, “I never attempt to make money on the stock market. I buy on the assumption that they could close the market the next day and not reopen it for five years.” It is this long-term mentality that separates value investors from those who follow the herd.

Principles of Value Investing

What to Look For

Value investors understand that fundamentals–such as earnings growth, dividends, cash flow, and book value–have a more significant impact on a stock’s price than market factors. If the fundamentals are sound, but the stock’s price is below its obvious value, the value investor knows this is a likely investment candidate; the market has incorrectly valued the stock. When the market corrects that mistake, the stock’s price should experience a boost. What about stocks that are down from a previous high? Say, a stock that is down 20% from its high of three months ago? Would this be a good investment? Possibly, but value investors are careful about stocks that experience a drop in price for a good reason. If there’s an obvious reason for the drop in price, it’s probably not a good candidate. When contemplating an investment, value investor Christopher H. Browne of Tweedy, Browne recommends asking yourself the following questions about a company’s future prospects: Can the company increase its revenue by a) raising prices? b) increasing sales? c) lowering expenses? d) selling or closing unprofitable divisions? e) growing the company? Who are the company’s competitors and how strong are they? Here are a few guidelines to follow:

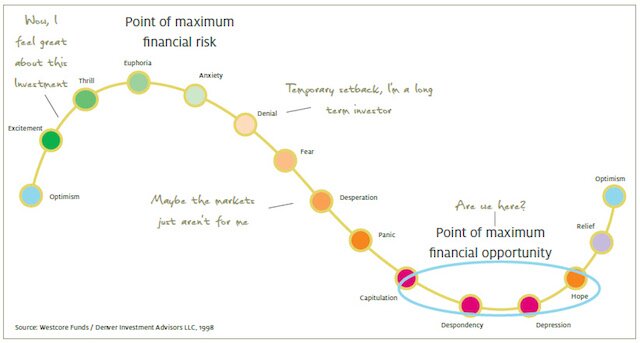

1. Don’t Panic

People tend to invest based on psychological biases rather than analysis of market fundamentals. They buy when the price of a particular stock is rising or when the value of the market as a whole appears to be rising. On the flip side, when the price of a particular stock is declining or when the value of the market as a whole appears to be falling, myopic loss aversion forces most people to sell their stocks. Instead of keeping their losses on paper and waiting for the market to change directions, they sell. The early 2000’s tech bubble and the mid-2000’s housing bubble were fueled by dramatic levels of overinvestment that bid up the prices of tech stocks and real estate beyond what the underlying companies and properties were worth. When the unsustainable highs began to fall, investors panicked and a crash ensued, causing some stocks to be priced closer to their true values and others to fall below their true values.

2. Small Name, Big Potential

Everyone wants to invest in the next big thing or even the current big thing. But that’s when herd mentality kicks in and ruins everyone’s chances. Look for companies that might sell for less than they’re worth because they’re under the radar. Small cap stocks, foreign stocks, and any other stocks that aren’t in the headlines or aren’t household names sometimes offer great potential but don’t get the attention they deserve.

3. A Weak Link

Sometimes a company has an unprofitable division that drags down its performance. If the company sells or closes that division, its financials can improve dramatically. Value investors who see this potential can buy the stock while its price is depressed and see gains later.

4. Seasonal Opportunity

It’s common for companies to go through periods of higher and lower profits. The time of year and the overall economy affect consumers’ moods and cause them to buy more or less. Their behavior might affect the stock’s price, but it has nothing to do with the company’s long term underlying value.

5. Stick With What You Know

To increase your odds of accurately answering these questions, it’s wise to buy companies that you understand. Companies that you understand will most likely be those in industries you have worked in or sell consumer goods products that you are familiar with. If you’ve worked for a biotech company for several years, you probably have a better-than-average understanding of the biotechnology business. And if you buy basic items like cars, clothes, appliances and food, you know a thing or two about consumer goods. Well-known investor Peter Lynch strongly advocated a strategy whereby retail investors can outperform institutions simply by investing in what they know before Wall Street catches on.

6. Lasting Demand

Another strategy that value investors favor is to buy companies whose products or services have been in demand for a long time and are likely to continue to be in demand. Looking at stock quotes won’t tell you which companies these are – you’ll have to do some critical thinking. Of course, it is not always possible to predict when innovation will make even a longstanding product or service obsolete, but we can find out how long a company has been in business and research how it has adapted to change over time. At this point it may be worthwhile to analyze management and the effectiveness of corporate governance to determine how the firm reacts to changing business environments.

Metrics and Ratios

Value investors should settle on a formula that works for them, but it will probably include as a minimum these elements:

- A Price Earnings Ratio (P/E) in the bottom 10 percent of its sector.

- A PEG of less than one. This indicates that the stock may be undervalued.

- A Debt to Equity Ratio of less than one.

- Strong earnings growth over an extended period. A realistic number might be in the 6% – 8% range over 7 to 10 years.

- A Price-to-Book ratio of one or less.

- Don’t pay more that 60% to 70% of the stock’s intrinsic per-share price.

P/E Ratio You’ve probably heard financial analysts comment that a stock is selling for some number “times earnings,” such as 30-times earnings or 12.5-times earnings. This means that P, the price the stock is currently trading at, is 30 times higher than E, the company’s annual earnings per share, or EPS. Value investors like the P/E ratio to be as low as possible, preferably even in the single digits. The number that results from calculating P/E is called the earnings multiple. Earnings Yield Earnings yield is simply the inverse of the earnings multiple. Since value investors like stocks with a low earnings multiple and earnings yield is the inverse of that number, we want to see a high earnings yield. A high earnings yield usually tells investors that the stock is able to generate a large amount of earnings relative to the share price.

Calculating Intrinsic Value

Coming up with the intrinsic value of a stock is a complicated process and there are a number of ways to get to the number. Fortunately, there are several places you can go on the Web to find the number. MorningStar.com calculates the number, which it calls “fair value,” on its site, however you need to be a member. Take the two-week free trial to see if you like their service. Another good source is Reuters, which also requires a registration, but it is free. Keep in mind, there is no “correct” intrinsic value. Two investors can be given the exact same information and place a different value on a company. For this reason, another central concept to value investing is that of “margin of safety.” For example, if you believe the intrinsic value is $40 per share, give yourself a margin of safety and lower the target to $36 per share. This ensures you’ll have some elbow room if your calculation is off. If you use one of the services mentioned above or another source to find the intrinsic value, determine if they have already factored in a margin of error.

The History

Value investing was developed in the 1920s at Columbia Business School by finance professors Benjamin Graham and David Dodd, authors of the classic text, Security Analysis. Graham and Dodd’s strategy was proposed as an alternative to the traditional method of relying on speculation and insider information, and asserted that the true value of a stock could be determined through research. Graham and Dodd’s security analysis principles provided the first rational basis for investment decisions, centering around the identification and sale of securities priced well below their true value. Graham began teaching his reason-based approach at Columbia Business School in 1928. For many years, he continually revised his methodology and his course, which he taught to both Columbia students and Wall Street professionals. The course was subsequently taught by his successor Roger F. Murray, who edited several editions of Security Analysis. Although the class was temporarily suspended when Murray retired in 1978, value investing was vigorously practiced by generations of investors who had studied with Graham or Murray throughout several decades. Some became legends in investment management, including Warren Buffett, Mario Gabelli, Glenn Greenberg, Charles Royce, Walter Schloss, and John Shapiro. Despite the vast and volatile changes in the economy and securities markets during the last several decades, value investing has proven to be the most successful money management strategy ever developed. Value investors’ success over the second half of the twentieth century proved not only the validity of the value approach, but its preeminence over even the most widely taught and practiced modern investment theory, which was developed in the 1950s and ’60s and remains dominant even today. In the early ’90s, Columbia Business School reinvigorated the investment management curriculum. At the request of Mario Gabelli, Roger Murray gave a highly successful series of guest lectures, and the Columbia Business School subsequently reintroduced value investing into the finance curriculum. The Robert Heilbrunn Professor of Finance and Asset Management was established, and Executive Education launched a value investing course that is consistently oversubscribed. The school also began the highly successful annual Graham & Dodd Breakfast. Held every fall, the breakfast draws many of the most distinguished figures in the investing profession. The Heilbrunn Center for Graham & Dodd Investing was established in 2001, ensuring a permanent home for value investing at Columbia Business School. With unmatched access to Wall Street, a renowned finance division, and the resources of the Heilbrunn Center, Columbia Business School offers an unparalleled program in investing. The birthplace of the value approach and security analysis, today the school is educating a new generation of investors. In 1984, Buffett returned to Columbia to give a speech commemorating the 50th anniversary of the publication of “Security Analysis.” During his speech, Buffett presented his own investment performance record as well as those of Bill Ruane, Tom Knapp and Walter Schloss. Each of these men, including Buffett, posted investment results that far exceeded the returns of the stock market indexes. Buffett noted that each of their portfolios varied significantly in the number and type of stocks, but every manager adhered to Benjamin Graham’s investment principles. The investment principles taught by Graham at Columbia University became legend in the field of professional stock analysis. Fortunately, Benjamin Graham made his principles easily accessible to all investors by writing the classic book, “The Intelligent Investor,” which Warren Buffett described as “by far the best book on investing ever written.” In “The Intelligent Investor,” Graham set forth the principles that form the foundation of value investing. Value investors seek to purchase undervalued stocks at prices that are clearly below the true or “intrinsic value” of a company.

Value investing was developed in the 1920s at Columbia Business School by finance professors Benjamin Graham and David Dodd, authors of the classic text, Security Analysis. Graham and Dodd’s strategy was proposed as an alternative to the traditional method of relying on speculation and insider information, and asserted that the true value of a stock could be determined through research. Graham and Dodd’s security analysis principles provided the first rational basis for investment decisions, centering around the identification and sale of securities priced well below their true value. Graham began teaching his reason-based approach at Columbia Business School in 1928. For many years, he continually revised his methodology and his course, which he taught to both Columbia students and Wall Street professionals. The course was subsequently taught by his successor Roger F. Murray, who edited several editions of Security Analysis. Although the class was temporarily suspended when Murray retired in 1978, value investing was vigorously practiced by generations of investors who had studied with Graham or Murray throughout several decades. Some became legends in investment management, including Warren Buffett, Mario Gabelli, Glenn Greenberg, Charles Royce, Walter Schloss, and John Shapiro. Despite the vast and volatile changes in the economy and securities markets during the last several decades, value investing has proven to be the most successful money management strategy ever developed. Value investors’ success over the second half of the twentieth century proved not only the validity of the value approach, but its preeminence over even the most widely taught and practiced modern investment theory, which was developed in the 1950s and ’60s and remains dominant even today. In the early ’90s, Columbia Business School reinvigorated the investment management curriculum. At the request of Mario Gabelli, Roger Murray gave a highly successful series of guest lectures, and the Columbia Business School subsequently reintroduced value investing into the finance curriculum. The Robert Heilbrunn Professor of Finance and Asset Management was established, and Executive Education launched a value investing course that is consistently oversubscribed. The school also began the highly successful annual Graham & Dodd Breakfast. Held every fall, the breakfast draws many of the most distinguished figures in the investing profession. The Heilbrunn Center for Graham & Dodd Investing was established in 2001, ensuring a permanent home for value investing at Columbia Business School. With unmatched access to Wall Street, a renowned finance division, and the resources of the Heilbrunn Center, Columbia Business School offers an unparalleled program in investing. The birthplace of the value approach and security analysis, today the school is educating a new generation of investors. In 1984, Buffett returned to Columbia to give a speech commemorating the 50th anniversary of the publication of “Security Analysis.” During his speech, Buffett presented his own investment performance record as well as those of Bill Ruane, Tom Knapp and Walter Schloss. Each of these men, including Buffett, posted investment results that far exceeded the returns of the stock market indexes. Buffett noted that each of their portfolios varied significantly in the number and type of stocks, but every manager adhered to Benjamin Graham’s investment principles. The investment principles taught by Graham at Columbia University became legend in the field of professional stock analysis. Fortunately, Benjamin Graham made his principles easily accessible to all investors by writing the classic book, “The Intelligent Investor,” which Warren Buffett described as “by far the best book on investing ever written.” In “The Intelligent Investor,” Graham set forth the principles that form the foundation of value investing. Value investors seek to purchase undervalued stocks at prices that are clearly below the true or “intrinsic value” of a company.

Famous Value Investors

Warren Buffet

Buffett was born in 1930. He was Graham’s student at Columbia and later his employee. Buffett thinks of buying stocks as buying companies (and is wealthy enough that he sometimes buys entire companies), and he has an indefinite time horizon for his investments. He made his first investment at age 14 and became a millionaire by around age 30. Along with Charlie Munger, he purchased a textile company called Berkshire Hathaway (NYSE:BRK.A, BRK.B) in 1965 and used the cash flows from the business to invest in companies such as Coca Cola (NYSE:KO) and American Express (NYSE:AXP) and to purchase entire companies such as GEICO. He has become one of the wealthiest men in the world through value investing.

Walter Schloss

Early in his career, Schloss worked with Buffett at Graham’s firm, Graham-Newman. In 1955, he started his own investment management firm. In 50 years as an investment manager, he averaged about 15% annual returns after fees. He uses company financial statements and the investment publication Value Line for much of his investment research. He looks for companies where management is a major stockholder, debt is low and the stock is trading at a discount to book value. Strategies he has used successfully include shorting stocks and holding large amounts of cash when he didn’t see good investment opportunities. He also diversified beyond what some value investors would recommend, sometimes owning more than 100 stocks at a time. Schloss also never went to college, proving once again that you don’t need a university degree to make lots of money and you don’t need to major in finance to become a great investor.

Christopher H. Browne

Browne worked at Tweedy, Browne Company, an investment firm founded by his father, Forrest Tweedy, for 40 years. Tweedy, Browne’s investment philosophy is based on Graham’s teachings. In fact, Graham traded through the company for three decades. Buffett was also a customer: it was through Tweedy, Browne that he purchased Berkshire Hathaway. The company also had a relationship with Schloss. Initially a brokerage, Tweedy, Browne became an investment firm in 1975 and later developed a handful of value-oriented mutual funds that have outperformed the S&P 500. n 1983 the company started investing in international value stocks. The company’s managing directors pride themselves on owning the same investments that they manage for their clients.

Criticism

Critics of value investing tend to focus on the fact that it’s difficult to predict stock trends for companies you don’t know well. This means you are stuck looking for businesses that you can easily understand because you have to be able to make an educated guess about the future earnings of the business. The more complex a business is, the more uncertain your projections will be. Other critics say it’s getting harder to predict trends in general. Professor Jeremy Siegel notes that accounting standards have changed in recent years, bringing the accuracy of value investing metrics into question. According to money manager Lonnie Rush, stock valuations are unusually compressed. In other words, stocks are trading in a much tighter price-to-earnings range than they have in the past, and there are relatively few stocks with very low ratios to be found. Why are things tougher to value these days? For one thing, business is much more complex than it used to be. With intellectual property rights, patents, and licensing fees, studying balance sheets is a bit murky. In addition, the days of sweating over spreadsheets are over. Computer programs and stock screeners make it simple to find a company that fits a certain mold– even the layman can whittle down enormous loads of data and draw conclusions. The advantage of having the fortitude to do the “hard work” is gone, lost in a sea of statistics and a market inundated with information. Another criticism of value investing is that it could potentially mislead retail value investors. This is because a low-priced stock, or a stock that saw a drop in its price significantly, could be due to a fundamental change in the company’s financial health. Then there is the issue of calculating “intrinsic value.” Some analysts believe that two investors can analyze the same information and reach different conclusions regarding the intrinsic value of the company, and that there is no systematic or standard way to value a stock. In other words, a value investing strategy can only be considered successful if it delivers excess returns after allowing for the risk involved, where risk may be defined in many different ways, including market risk, multi-factor models, or idiosyncratic risk. In specific industries, such as the area of technology, value investing can be tricky. Everett Rogers’ theory on the diffusion of innovation asserts that the adoption of new technologies follows a bell curve comprised of innovators (2.5%), early adopters (13.5%), early majority (34%), late majority (34%) and laggards (16%). The cumulative adoption of technology over time generates what is known as the S-curve. Over the last 100 years, technology adoptions have always followed this same S-curve, leading to market saturation. What has changed significantly in recent years is the rate of adoption. While technologies from the early part of the century like electricity, automobiles, and the telephone took well over 50 years to reach 50% adoption, newer technologies like Internet, PCs, smartphones, and tablets are being adopted much faster. The flip side of this is when new technologies are adopted faster, incumbent solutions die faster. Quicker adoption leads to quicker destruction of old technologies. Businesses that refuse to embrace or adapt don’t just slowly decline; they fall off a cliff and take their cash flows with them. This makes for risky value investing.

Pitfalls to Avoid

Basing Your Calculations on the Wrong Numbers

Since value investing decisions are partly based on an analysis of financial statements, it is imperative that these calculations be performed correctly. Using the wrong numbers, performing the wrong calculation or making a mathematical typo can result in basing an investment decision on faulty information.

Overlooking Extraordinary Gains or Losses

Some years, companies will experience unusually large losses or gains from events such as natural disasters, corporate restructuring or unusual lawsuits and will report these on the income statement under a label such as “extraordinary item – gain” or “extraordinary item – loss.” When making your calculations, it is important to remove these financial anomalies from the equation to get a better idea of how the company might perform in an ordinary year.

Ignoring the Flaws in Ratio Analysis

The problem with financial ratios is that they can be calculated in different ways. Here are a few factors that can affect the meaning of these ratios:

- They can be calculated with before-tax or after-tax numbers.

- Some ratios provide only rough estimates.

- A company’s reported earnings per share (EPS) can vary significantly depending on how “earnings” is defined.

- Companies differ in their accounting methodologies, making it difficult to accurately compare different companies on the same ratios.

Overpaying

One of the biggest risks in value investing lies in overpaying for a stock. When you underpay for a stock, you reduce the amount of money you could lose if the stock performs poorly. The closer you pay to the stock’s fair market value – or even worse, if you overpay – the bigger your risk of losing capital.

Not Diversifying

Benjamin Graham suggests 10 to 30 companies is enough to adequately diversify. On the other hand, the authors of “Value Investing for Dummies, 2nd. ed.,” say that the more stocks you own, the greater your chances of achieving average market returns. They recommend investing in only a few companies and watching them closely.

Listening to Your Emotions

Once you have purchased the stock, you may be tempted to sell it if the price falls. You must remember that to be a value investor means to avoid the herd-mentality investment behaviors of buying when a stock’s price is rising and selling when it is falling.

Not Comparing Apples to Apples

Comparing a company’s stock to that of its competitors is one way value investors analyze their potential investments. However, companies differ in their accounting policies in ways that are perfectly legal. When you’re comparing one company’s P/E ratio to another’s, you have to make sure that EPS has been calculated the same way for both companies. For more information on value investing, check out the following resources:

- Value Investing vs Modern Portfolio Theory:

- Graham, Benjamin (1934). Security Analysis New York: McGraw Hill Book Co., 4. ISBN 0-07-144820-9.

- Graham (1949). The Intelligent Investor New York: Collins, Ch.20. ISBN 0-06-055566-1.